Retired public sector employees, members of countless unions, and advocacy group leaders are celebrating this month because nearly three million Americans are about to receive higher Social Security payments thanks to the Social Security Fairness Act signed into law by President Joe Biden on January 5, 2025.

This new legislation restores Social Security benefits for public sector retirees and their spouses by repealing the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO).

For more than 40 years, WEP and GPO reduced Social Security benefits for public-sector retirees who had Social-Security-tax-exempt pension benefits from a public employer. The individuals affected included retired teachers, police officers, firefighters, and their spouses across several states.

While it is unclear when these changes will go into effect, individuals need to understand how these changes will impact their retirement plans. Additionally, financial advisors can begin preparing their clients for these changes now.

Understanding WEP and GPO

WEP and the current iteration of GPO were put into place in 1983 as a way to limit the Social Security benefits being paid out to public sector employees who received federal, state, or local pensions and who did not pay into the Social Security program.

In other words, these original provisions were created to reduce the amount of Social Security benefits paid out to individuals who also had money available in pensions, thus, leading to these individuals receiving an unintentional "windfall" due to the formula used to calculate Social Security benefits — a formula designed to benefit lower-income workers and their spouses.

“It’s always been bit of a wealth distribution program which favors lower income workers.” says David Freitag, a financial planning consultant and Social Security expert for MassMutual.

The amount that WEP and GPO reduced Social Security payments was based on the number of years that an individual paid Social Security taxes. The fewer years one paid into Social Security, the greater the reduction.

Benefit Reductions Under WEP

Under WEP, the index used in the formula for calculating Social Security benefits could be reduced to 40% (from a 90% index) for public-sector retirees, resulting in a maximum offset of $587.

While the reduction wasn't insignificant, individuals subject to WEP reductions would still receive some Social Security benefits monthly.

Benefit Reductions Under GPO

GPO reduced Social Security benefits for widows and widowers by two-thirds of the amount of the spouse's non-Social-Security-covered pension.

For example, a widow qualifying for $1,200 in Social Security spousal benefits who also received $600 per month from a non-covered pension would receive a reduced spousal benefit of $800.

Referring to the severity of GPO reductions, Freitag says, "This could be up to 100% of anything you would be eligible to collect from your spouse, [a] very much more punitive type of offset."

Under GPO, spouses with government pensions could be subject to losing all of a widow's or widower's benefits, depending on the size of their pension benefits and the amount of their deceased spouse's Social Security payments.

Why the New Legislation?

Although WEP and GPO were designed to safeguard Social Security program funds by limiting payments, the provisions led to unintended consequences that unfairly penalized individuals and spouses of individuals with short or low-paying public-sector careers.

Throughout the past decades, retirees, unions, politicians, and advocacy agencies — such as The National Active and Retired Federal Employees Association — have been fighting and lobbying to get these provisions repealed.

Key Provisions of the Social Security Fairness Act

The elimination of WEP and GPO will mean drastic improvements to Social Security benefits for retirees and surviving spouses who were previously impacted by the offsets.

According to estimates from the Congressional Budget Office, eliminating WEP could increase monthly payments by an average of $360, while eliminating GPO could increase monthly payments by an average of $700 or $1,190, respectively, for individuals with living spouses or widows/widowers.

In addition to fully restoring all future benefits, the Social Security Fairness Act will retroactively reimburse benefits payable after December 2023.

Serving more people than ever before, the Social Security Administration (SSA) is currently stymied by the lowest staffing levels in 50 years and a hiring freeze. The SSA currently reports no plan or official timeline for implementing the Social Security Fairness Act.

However, the legislation is law, and payment changes are anticipated to go into effect by the end of 2025. The SSA encourages all public-sector retirees to ensure that their my Social Security accounts reflect their current bank account and mailing information.

The Social Security Fairness Act and Its Implications for Retirement Planning

The Social Security Fairness Act is restoring fairness and equality to public-sector employees and their spouses, ensuring they receive the full benefits they have worked hard to earn throughout their careers by also restoring full benefit payments.

The new legislation restores benefits for about 750,000 individuals impacted by WEP and 2.1 million spouses impacted by GPO. Individuals who were previously subject to WEP could receive an increase of up to $587 in their monthly payments, while individuals who were previously subject to GPO could receive even more significant benefit adjustments.

In response to these impending changes, financial planners working with public-sector employees like teachers and first responders should proactively reassess their clients' retirement strategies to provide them with options for leveraging their increased benefits and revising their current financial plans.

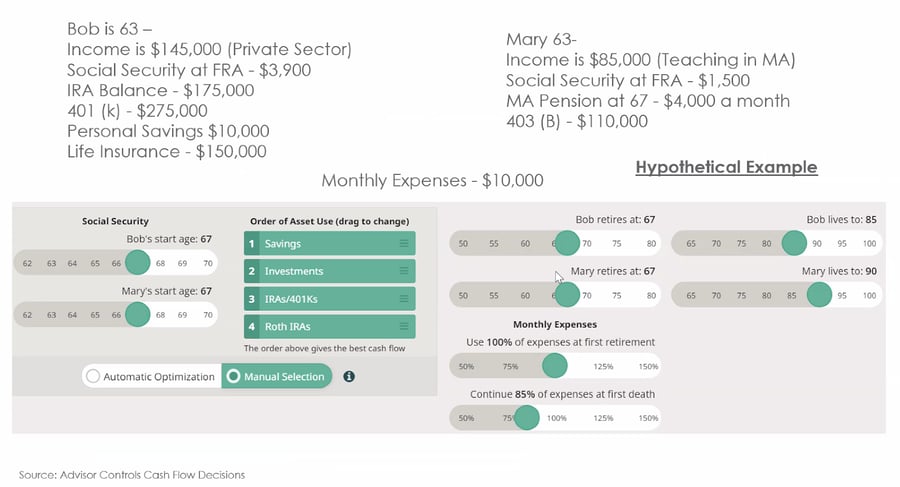

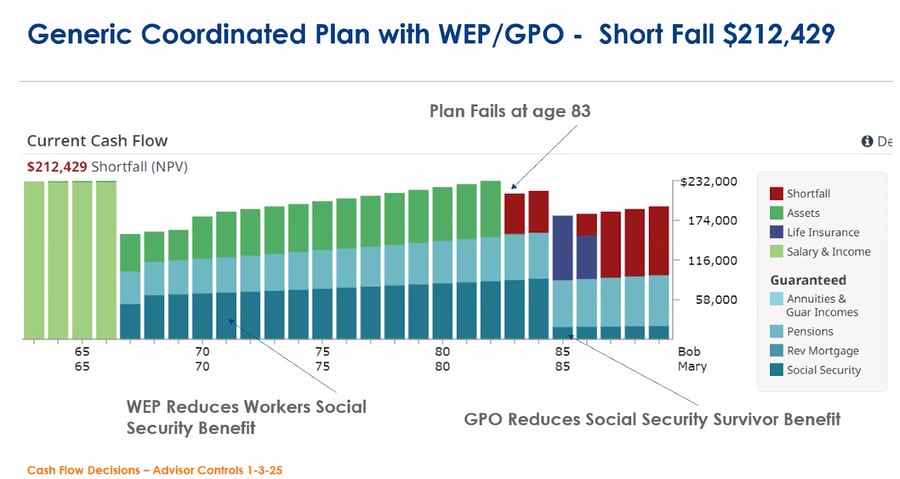

How Advisor Controls' Cash Flow Decisions Tool Can Help

Financial advisors use several data points such as income, Social Security at full retirement age (FRA), pension at FRA, estimated life expectancy, savings, life insurance, and expected future cost of living to create financial models for their clients.

With all of these separate data points, it can be difficult for clients to understand how the Social Security Fairness Act will impact their retirement and affect their financial strategy.

Financial advisors with expertise in Excel and plenty of free time could manually design complicated spreadsheets to work out these financial models — but these complex, detailed, and advanced manual processes are not necessary with Cash Flow Decisions from Advisor Controls.

"What [financial advisors] need is a conceptual tool that will let a client understand what just happened, and that's what this is," says Freitag. "What [Cash Flow Decisions] does is help visualize the issue."

Cash Flow Decisions allows financial advisors to input basic data points for clients, shift sliders to adjust assumptions, and manipulate individual points (such as a radio button to add or remove GPO and WEP provisions).

Cash Flow Decisions automatically applies thousands of Social Security rules and executes hundreds of calculations to map out a client's potential financial future.

Advisors can manipulate the data points and change assumptions to seamlessly demonstrate different possible paths and options to clients, helping them select the best strategy for maintaining their lifestyle and achieving their retirement goals.

"Literally, with the movement of one key on the Cash Flow Decisions tool, you can make [a client] feel much better about their future," says Freitag.

In short, Cash Flow Decisions enables financial advisors to quickly determine the difference in Social Security benefits for clients before and after the Social Security Fairness Act with the single click of a button.

Next Steps for Financial Planners: What You Can Do to Guide Your Clients Through This Change

The Social Security Fairness Act brings positive changes for previously affected public-sector retirees and their spouses.

Financial advisors have the opportunity to share this good news with their clients and highlight the potential benefits for their future. However, before doing so, advisors must first identify which clients will be impacted by the new legislation.

The Social Security Fairness Act will affect all current and future clients who earned (or are earning) income in a public-sector job in an affected state. The list will include all existing clients who have a WEP or GPO provision factored into their existing financial plan.

Freitag reminds all financial advisors that "the purpose of the discussion is not to tell people what to do but to show them what their choices are."

In addition to demonstrating the impact fully restored Social Security benefits will have on retirement, financial advisors can also leverage the murky implementation timeline to increase and improve communications with clients.

For example, advisors can keep clients informed as new updates are released and even help them update their information with the SSA to ensure prompt reimbursement and payment once the new provisions are in place.

Future Outlook: The Long-Term Impact of the Social Security Fairness Act

The Social Security Fairness Act improves equality and benefits for countless public-sector employees whose hard work teaching, protecting, and serving has benefited countless communities across the United States.

That said, this legislation places a drastically increased strain on the Social Security program's funding. While money currently exists in a Social Security trust, new provisions will worsen existing insolvency. A solution for filling the funding gap has yet to be determined or publicly discussed.

Due to funding challenges, new legislation will likely be created to address concerns and preserve the Social Security program. These changes may require revisiting clients’ retirement forecasts to adjust financial planning models and money management strategies.

Streamline Retirement Planning for Your Clients With Cash Flow Decisions

Advisor Controls is dedicated to equipping financial planners with the tools and insights needed to help their clients navigate changes like those caused by the Social Security Fairness Act.

With our Cash Flow Decisions tool, financial advisors can effectively update their clients' financial plans with easily visualized projections.

Staying ahead of future financial advising trends and evolving regulations, we are committed to leading the financial planning software industry into the future. By ensuring our clients are always ahead of the curve, we take pride in navigating the ever-changing landscape of rules, regulations, and legislation

Get a Free 14-Day Trial of Cash Flow Decisions